When Rates Matter More Than Prices

Home prices often take center stage in conversations about affordability. This month’s data, however, points to a different story. Over the past nine years, Denver’s median sales price has increased at an average annual rate of approximately 6%, a pace that closely mirrors the market’s long-term historical trend. Even the dramatic ups and downs of the pandemic era ultimately settled back into that same trajectory. What has changed more significantly is the cost of borrowing money. Mortgage rates remain well above the levels many homeowners became accustomed to, creating a meaningful gap between what buyers can afford and what current homeowners are willing to give up. As a result, market activity appears to be influenced less by home prices themselves and more by the cost of making a move.

Home prices often take center stage in conversations about affordability. This month’s data, however, points to a different story. Over the past nine years, Denver’s median sales price has increased at an average annual rate of approximately 6%, a pace that closely mirrors the market’s long-term historical trend. Even the dramatic ups and downs of the pandemic era ultimately settled back into that same trajectory. What has changed more significantly is the cost of borrowing money. Mortgage rates remain well above the levels many homeowners became accustomed to, creating a meaningful gap between what buyers can afford and what current homeowners are willing to give up. As a result, market activity appears to be influenced less by home prices themselves and more by the cost of making a move.

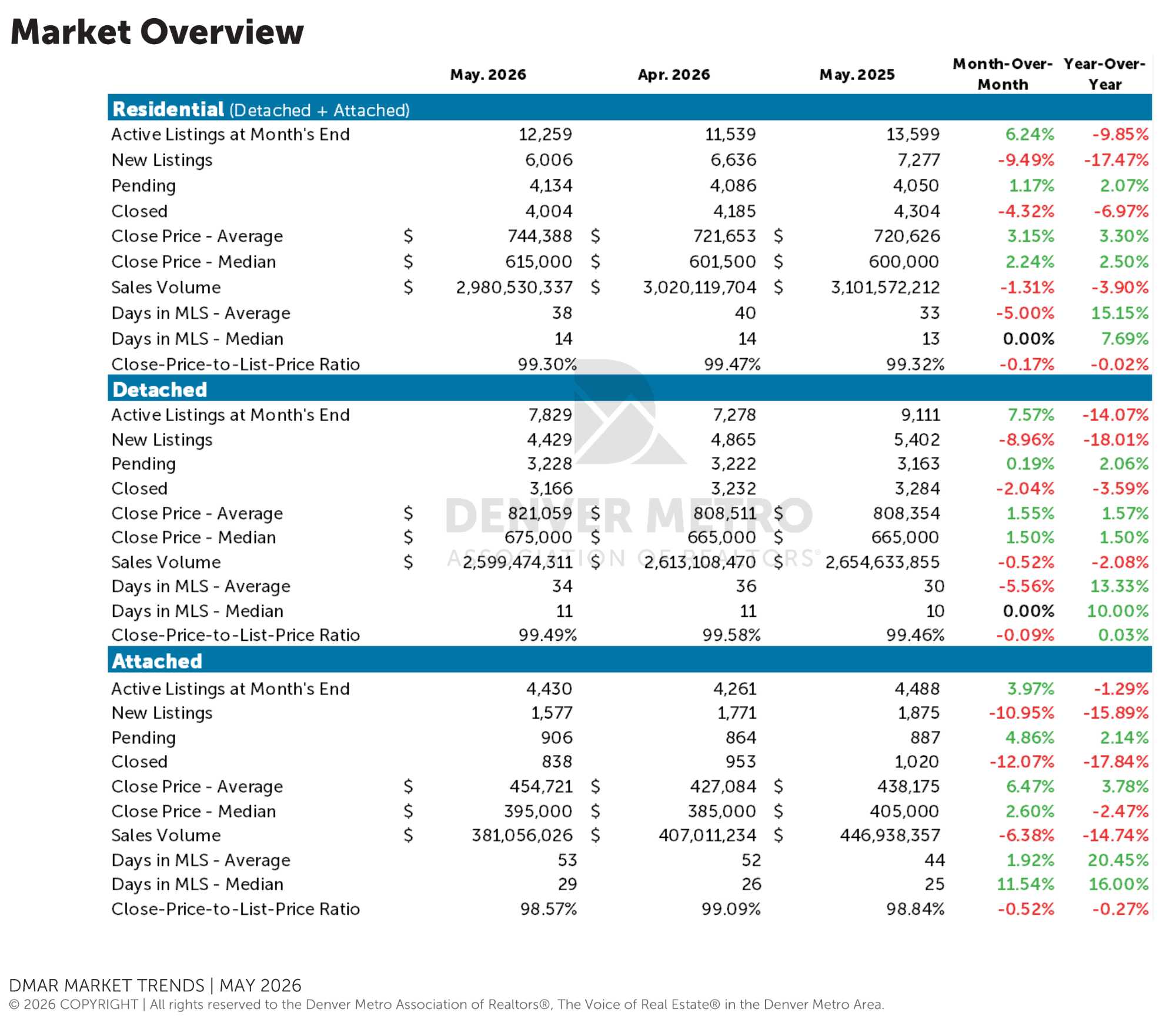

Inventory continued to grow in May, though at a slower pace than we typically see during the spring market. Active listings at month’s end reached 12,259 homes, increasing 6.24% from April but falling below the historical May average increase of 9.38%. New listings declined across both detached and attached homes, and inventory levels remain below where they were this time last year. Active inventory continued to rise despite fewer new listings coming to market, suggesting homes are taking longer to sell rather than being offset by a wave of new supply. Combined with slightly lower transaction volume than last year, this may reflect homeowners remaining hesitant to trade a low mortgage rate for a significantly higher one.

Days in MLS remained relatively steady in May. Average days on market dipped slightly to 38 days, while the median remained unchanged at 14 days. Detached homes saw modest improvements from April, while attached homes experienced small increases in both average and median days on market. Compared to last year, homes across all segments are generally taking longer to sell. Buyers continue moving quickly on homes that are thoughtfully prepared and aggressively priced, while homes positioned more moderately are often taking closer to the market average before securing a contract.

Buyer activity improved modestly in May. Pending sales increased slightly from April overall, with attached homes seeing the strongest gains. Closed sales, however, moved in the opposite direction, declining across all segments of the market. Compared to last year, pending activity remains slightly higher while closed sales continue trailing 2025 levels. Buyers are still participating in the market, while elevated mortgage rates continue creating friction throughout the transaction process.

Pricing remained remarkably steady in May. Average and median sales prices both posted modest gains from April, bringing the overall average close price to $744,388 and the median price to $615,000. Year over year, appreciation remains relatively modest and closely aligned with the market’s longer-term trend. The data continues supporting the idea that prices are behaving much as they historically have, despite the challenges many buyers and sellers are facing.

For Sellers

While inventory remains relatively constrained by historical standards, buyers are becoming increasingly selective. Homes that are thoughtfully prepared, strategically marketed, and priced aggressively continue attracting strong interest. Sellers should also pay close attention to factors that impact affordability. Properties with solar leases, for example, may face additional scrutiny from buyers who are already stretching their budgets. In some situations, paying off a solar lease before listing or at closing may help reduce friction during negotiations and broaden the pool of interested buyers.

For Buyers

Today’s market may feel challenging, yet the data suggests affordability concerns are being driven more by mortgage rates than by home prices themselves. Rather than waiting for a significant price correction, buyers may benefit more from exploring financing strategies such as temporary rate buydowns, seller concessions, or future refinancing opportunities. A meaningful decline in rates can have a much larger impact on monthly payments than a modest change in home prices.

Healthy Housing Market Meets the High Cost of Financing

The data continues pointing toward a market that is functioning much as it should. Inventory is growing, buyers remain active, and home values continue following a relatively predictable path. For many households, the greater challenge is not the price of the home itself; it is the cost of financing it. That distinction may not lower the monthly payment. It does, however, help explain why transaction volume remains muted despite an otherwise healthy market. In many ways, today’s market feels less constrained by housing fundamentals and more constrained by the cost of accessing them.

(Info Source: D.M.A.R. (The Denver Metro Association of Realtors, YCRE Analysis)

*We use reasonable efforts to include accurate and up-to-date information. The real estate market changes often. We make no guarantees of future real estate performance and assume no liability for any errors of omission in the content.