Spring’s Early Rush Gives Way to Stability

After several months of steadily building momentum, April’s market data suggests the spring market may be beginning to settle into a more familiar rhythm. Inventory climbed significantly, while pending activity softened slightly and pricing remained relatively stable overall. Combined with the unusually mild winter and early start to the spring market we experienced this year, some of the typical seasonal surge may have simply arrived earlier than usual. While earlier months left some question as to whether this was temporary seasonal momentum, the market continues showing many of the same patterns we’ve consistently seen since 2022: stable pricing, measured buyer activity, and gradually increasing inventory.

After several months of steadily building momentum, April’s market data suggests the spring market may be beginning to settle into a more familiar rhythm. Inventory climbed significantly, while pending activity softened slightly and pricing remained relatively stable overall. Combined with the unusually mild winter and early start to the spring market we experienced this year, some of the typical seasonal surge may have simply arrived earlier than usual. While earlier months left some question as to whether this was temporary seasonal momentum, the market continues showing many of the same patterns we’ve consistently seen since 2022: stable pricing, measured buyer activity, and gradually increasing inventory.

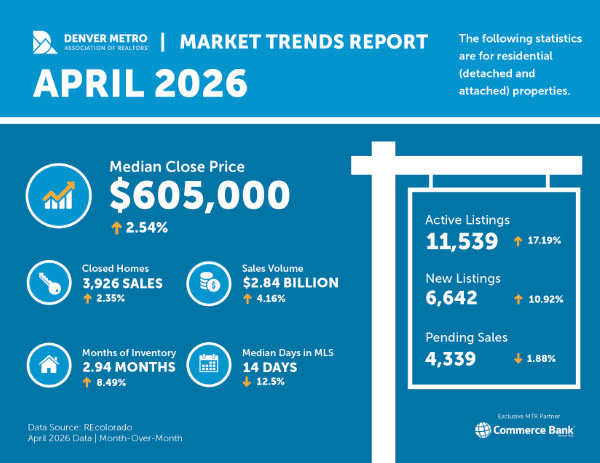

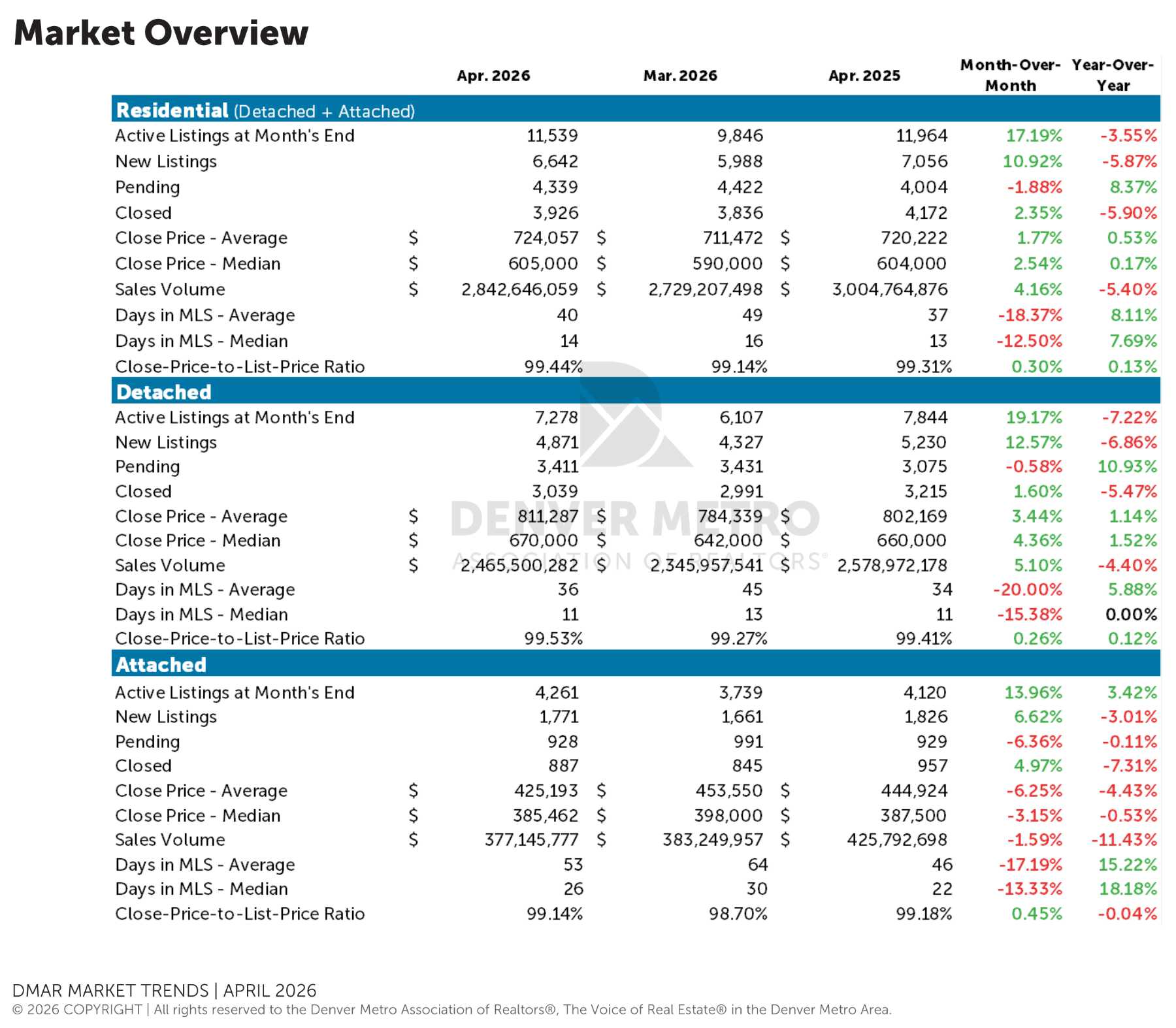

Inventory saw one of its largest jumps of the spring so far, with active listings at month’s end climbing to 11,539 homes. New listings also increased notably from March, particularly in the detached market. Compared to last year, inventory remains meaningfully higher across most segments of the market. While inventory levels are still below long-term historical averages, buyers are continuing to gain more options as the market moves deeper into the spring season. The combination of rising inventory and slightly softer pending activity suggests homes may simply be absorbing at a slower pace than they were earlier this year.

Even with inventory increasing, homes moved through the market more quickly in April. Average and median days in MLS both declined notably from March, with detached homes continuing to outperform the attached market overall. Compared to last year, however, homes are still generally taking longer to sell across all property types. Buyers continue moving quickly on homes that are priced and positioned aggressively, while homes priced more moderately are often taking closer to the market average before securing a buyer.

Pending sales softened slightly in April after several months of stronger gains, while closed sales still increased modestly from March overall. Detached activity remained relatively steady, while the attached market experienced a more noticeable slowdown in pending contracts. Compared to last year, pending sales remain higher overall, signaling that buyers are still active despite the recent moderation in momentum. Closed sales continue trailing last year’s pace, likely reflecting the lag between contracts being signed and final closings occurring.

Pricing remained remarkably steady in April. Average and median close prices both posted modest gains from March, bringing the average close price to $724,057 and the median to $605,000 overall. Detached homes continued showing slightly more strength, while attached homes experienced a bit more softness compared to last year. Overall pricing, however, has remained relatively flat year over year, reinforcing the broader theme of stability rather than rapid appreciation or decline. Sellers are still achieving very strong pricing relative to list price, with homes closing at an average of 99.44% of asking price.

For Sellers

Pricing strategy matters more than it has in recent years. Homes that are thoughtfully prepared, aggressively priced, and marketed strategically are still moving quickly, while buyers now have enough options that moderate pricing or modest presentation can quickly slow momentum. Sellers hoping to secure a contract faster than the market averages will likely need to price aggressively from the start.

For Buyers

This market continues offering more opportunity and flexibility than we’ve seen in recent years. Increased inventory is creating more choice and slightly more negotiating leverage in certain situations, while pricing overall has remained relatively stable. At the same time, desirable homes are still moving quickly, reinforcing the importance of being prepared when the right property hits the market.

Stability is not stagnation

Rising inventory and flatter pricing trends continue pointing toward a market that is finding balance rather than losing momentum. Buyers have more options, sellers are still achieving strong results when homes are positioned strategically, and the market continues rewarding preparation, pricing discipline, and patience on both sides of the transaction.

(Info Source: D.M.A.R. (The Denver Metro Association of Realtors, YCRE Analysis)

*We use reasonable efforts to include accurate and up-to-date information. The real estate market changes often. We make no guarantees of future real estate performance and assume no liability for any errors of omission in the content.